It’s no secret that tons of people are nearing the age at which they’d like to retire and simply can’t do it. When they run retirement projections themselves or with a financial planner the numbers just don’t work. The projections are showing them outliving their money and being forced to live solely on social security.

In this case, to make a significant improvement in their retirement projections they can do one of two things:

- They could reduce their expected expenses in retirement

- They could work longer

I warn against choosing the first option. Yes, you could take fewer vacations, spend less on your grandchildren and play less golf but there are also other expenses you simply cannot control. Medical bills, house repairs, car accidents, etc. The second option, working longer, provides guaranteed benefits. By working longer you benefit in four different ways:

- You have less years of retirement to fund

- You have additional years of income (usually close to your peak earnings)

- You have more years to save in retirement accounts (and to receive employer matches)

- Your social security benefit will likely increase

It’s not the ideal situation, especially if you’re not in a job or career that you particularly enjoy. But by sacrificing a year or two of more work you can ensure yourself a much more enjoyable retirement.

Let’s examine a case study to determine how effective working just one more year has on a couple’s retirement projections.

Mark and Susan are married and both turn 65 this year and plan on retiring. Mark has a 401(k) with a value of $750,000 and will receive a monthly social security retirement benefit of $2,527 at his full retirement age of 66. Susan has a 401(k) with a value of $250,000 and a monthly social security retirement benefit of $1,813 at her full retirement age of 66. Since they are retiring at age 65 they have decided to take social security a year earlier than their full retirement ages which reduces their benefits to $2,359 and $1,692, respectively. With no debt they believe they can live comfortably on $100,000 of income during retirement with a 3% cost of living adjustment per year. Both of their families have histories of long healthy lives and they expect to live 30 years after retiring until age 95. Here is what a very simple retirement projection would look like modeled in Excel:

Mark and Susan end up depleting their 401(k) balance at age 92 and will be forced to live solely on social security for the remainder of their lives. Of course, this is assuming we are 100% correct on all our assumptions, which won’t be the case. A 6% growth rate in their 401(k), a 3% annual increase to social security and their expenses, and the fact that they both live at least to age 93 or longer. Numerous things could happen to throw off these projections. Abnormal investment returns in either direction, an early death for one or both spouses, or really high inflation or an extended period of deflation. The point is, doing the best we can on our projections, it seems that not outliving their money will be a close call.

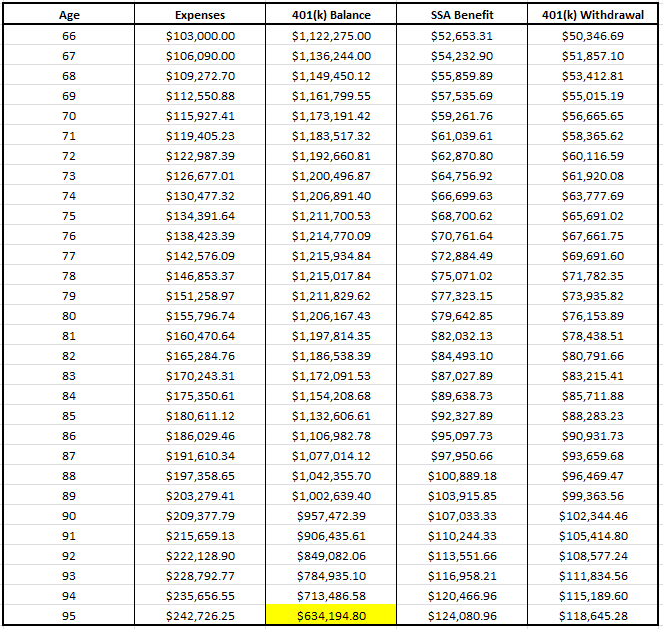

If Mark and Susan decide to work just one more year and retire at age 66 instead of 65 it’s incredible how different their projections look. Let’s re-cap the four benefits that occur by working longer and how they specifically benefit Mark and Susan’s situation.

- Less years in retirement to fund

Instead of funding 30 years of retirement, Mark and Susan will only be funding 29 years of retirement.

- Additional years of income

In Mark and Susan’s case let’s assume they make a joint income of $215,000. A very realistic number considering they’ve both worked the majority of their lives. Mark earns $150,000 and Susan earns $65,000.

- More years to save in retirement accounts

With good incomes, no debt, and no dependents to take care of Mark and Susan have the capacity to both max out their 401(k)s at $24,000 apiece. In addition they both receive an employer match of 5% that vests immediately. Assuming a 6% growth rate, this increases their combined 401(k) balances by $122,275.

- Social security benefit will increase

Since social security benefits are based on the top 35 years of earnings adjusted for inflation, Mark and Susan will be replacing one of their lower earnings years with this additional year of earnings. This will slightly increase their retirement benefit. However, they will receive a larger bump because they can afford to hold off on taking social security for one extra year. In this case they each get a 6.67% increase in their benefit for waiting until full retirement age. The higher earning year plus waiting until full retirement age to take benefits increases their total combined annual benefit by $3,165.

Although these changes may seem small it makes a significant difference in their projections.

By waiting one extra year to retire Mark and Susan are able to begin retirement with a higher 401(k) balance and social security benefit. This results in them taking less from their 401(k) each year which allows compound growth to work its magic. It all combines to give them some cushion in their retirement planning and projections. These new projections show them dying at age 95 with a balance of $634,194 in their 401(k)s.

Keep in mind this is just a case study, every situation is different and so will be the effect of working longer.

However, the point is, working even one year longer has multiple benefits on the longevity of your retirement capital and should be something you consider if you find yourself not fully prepared to retire at your desired age.